Feature Articles

Have a topic request or want to submit an article? Contact the MAGNIFYI Editors

The Texas Advantage: How Real Competition Transforms Energy Markets

Most conversations about competitive energy markets start with the same question: Are they working?

Too often, the answer is framed through residential switching rates or customer participation levels. And in many markets, those numbers tell an incomplete—and sometimes misleading—story.

Because competitive markets aren’t static.

They don’t simply succeed or fail.

They evolve.

Nowhere is that evolution more visible than in Texas.

Over the past decade, the Texas retail electricity market has moved through distinct phases—from rapid expansion and supplier entry to consolidation and scale. And in doing so, it has created something few markets have fully achieved:

A durable, competitive market that delivers real choice to consumers.

What the Data Shows

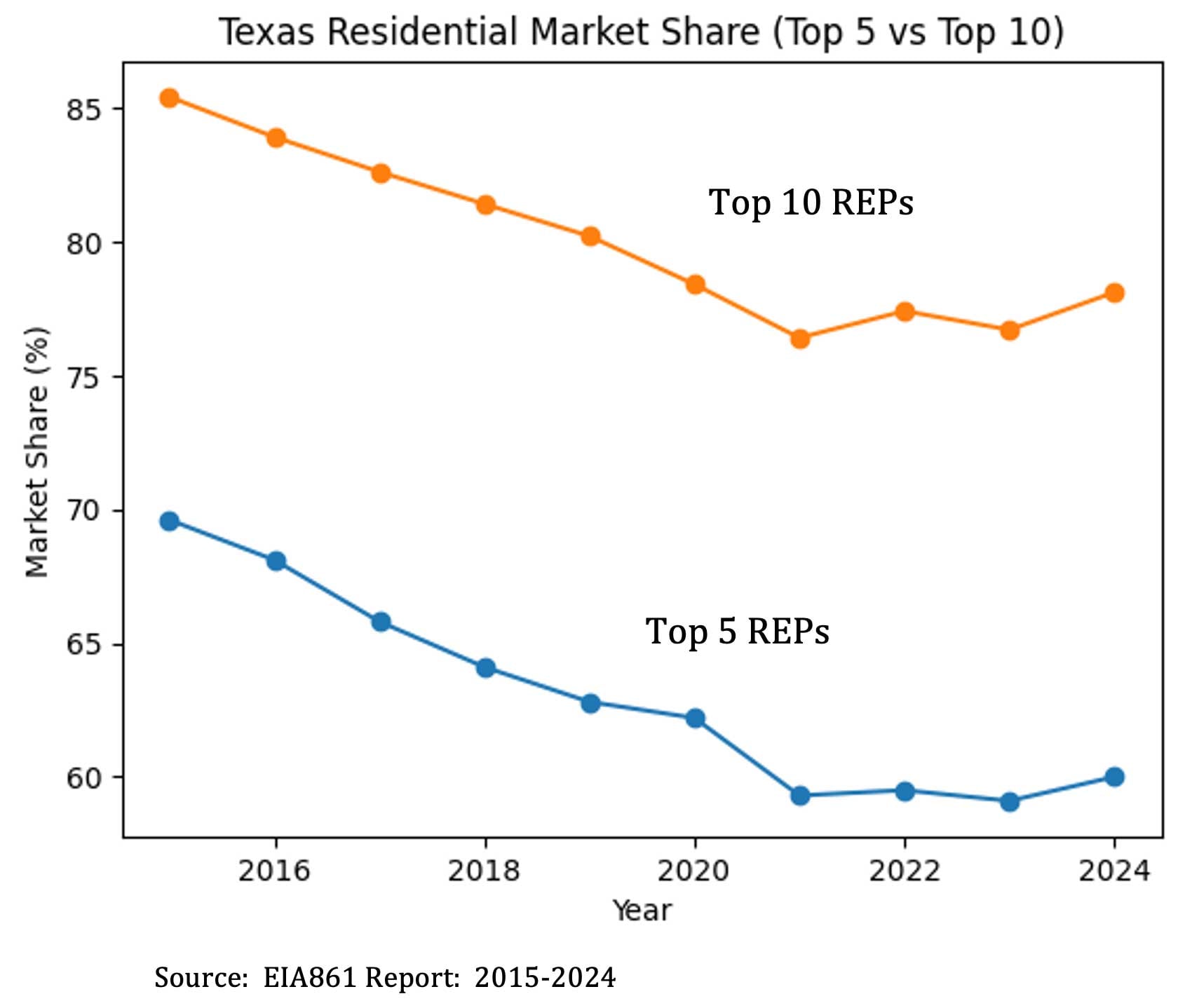

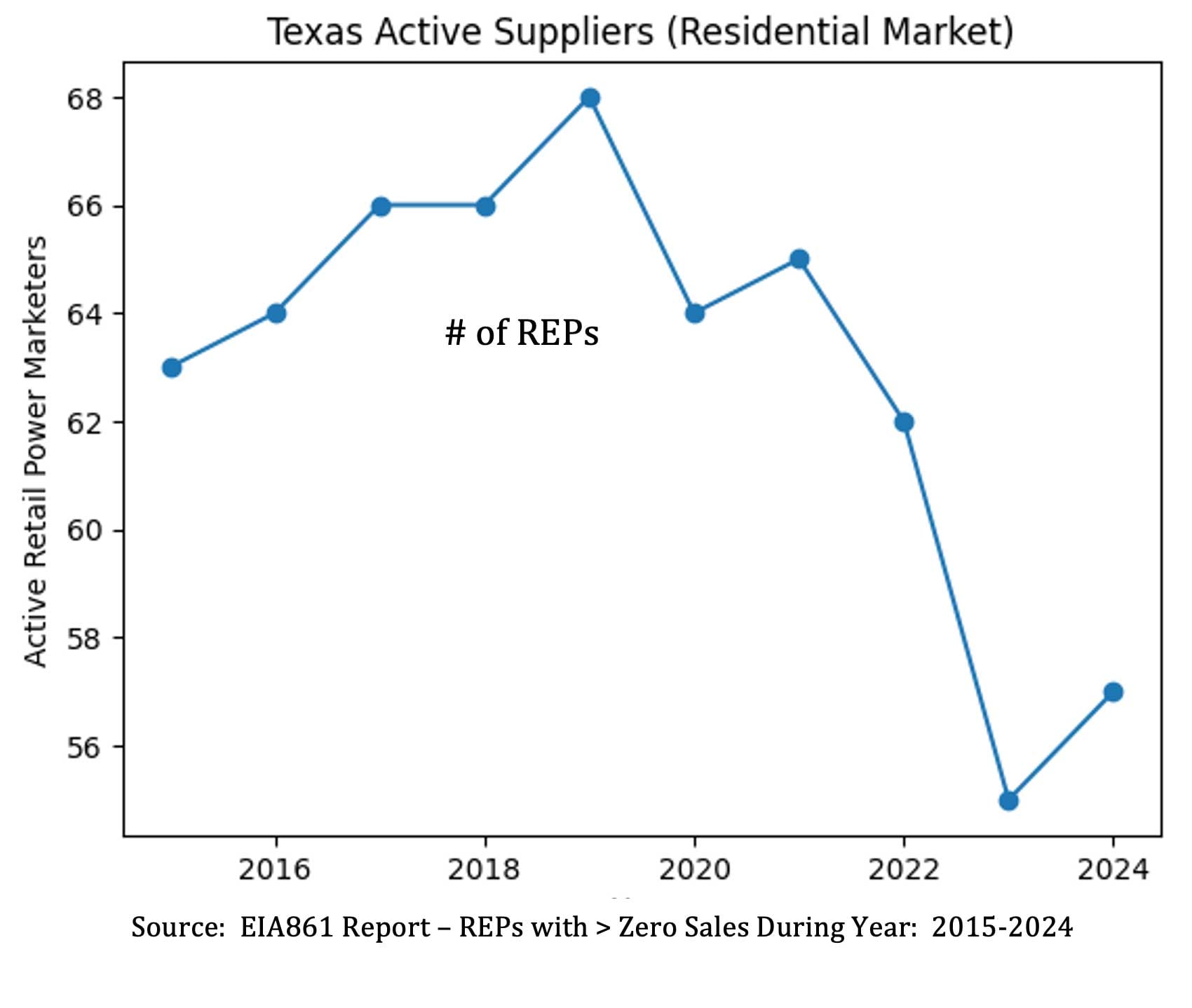

Analyzing the Texas residential electricity market from 2015 to 2024 reveals several clear trends.

Market concentration among the Top 5 largest suppliers has declined from ~70% to ~60% and from the mid-80% range to the high-70% range for the Top 10.

At the same time, the number of active retail power marketers over the past 10 years has declined from the mid-60s to the mid-50s.

And while concentration declined for much of the decade, the two largest suppliers—Reliant and TXU—have stabilized their combined share at 43.0%, up from 41.0% in 2021 but down from the 10 year high of 46.4% in 2015.

At first glance, these trends appear contradictory.

** Texas Residential Market Share (Top 5 vs Top 10)

** Active Retail Power Marketers (Residential Market)

The Role of Consolidation

The explanation is straightforward: the market has matured.

Early growth brought new entrants and fragmentation. More recently, smaller or less efficient suppliers have exited or sold customer portfolios.

Larger suppliers have acquired these books of business, increasing share through consolidation rather than purely organic switching.

Why Texas Is Different

Texas operates without a traditional utility default service model. Customers must actively choose a supplier, creating a fully competitive environment.

This structure enables both expansion and consolidation phases to fully develop—and ultimately delivers a broader, more dynamic set of choices to consumers.

Conclusion

The Texas retail electricity market offers a clear and important lesson.

Competitive energy markets do not remain in a constant state of expansion. They mature. They consolidate. And over time, stronger, more efficient suppliers emerge.

But that evolution should not be mistaken for a loss of competition.

In Texas, competition is not defined by the number of suppliers alone. It is defined by the breadth of choice available to consumers.

Customers can choose from:

- dozens of competing suppliers

- a wide range of pricing structures

- innovative products and value-added services

That level of choice—enabled by a market structure that does not rely on a utility-controlled default provider—is what sets Texas apart.

Even as the number of suppliers has declined, the market continues to deliver what competitive energy was designed to provide: meaningful options, transparent pricing, and the ability for consumers to select the product that best fits their needs.

Other competitive markets should take notice.

Because what is unfolding in Texas is not a sign of weakness.

It is a sign of success.