Feature Articles

Have a topic request or want to submit an article? Contact the MAGNIFYI Editors

The Untold Story of Competitive Energy Markets: Why the Commercial Market Thrived While Residential Lagged

The debate over competitive electricity markets often focuses on one statistic: how many residential customers have switched suppliers.

In many states, the answer is less than one-third. When measured by electricity consumption, the picture looks largely the same. The share of residential electricity served by competitive suppliers closely tracks the share of households that have chosen a competitive supplier, indicating that residential participation remains modest.

But that statistic tells only part of the story.

Using data from the U.S. Energy Information Administration’s EIA‑861 survey, a different picture emerges when electricity markets are measured by the share of load served by competitive energy suppliers versus investor‑owned utilities providing bundled default service. This approach compares electricity supplied by Retail Power Marketers (competitive suppliers) with electricity supplied by Investor Owned Utilities under bundled service, rather than relying solely on switching statistics commonly used in retail market studies.

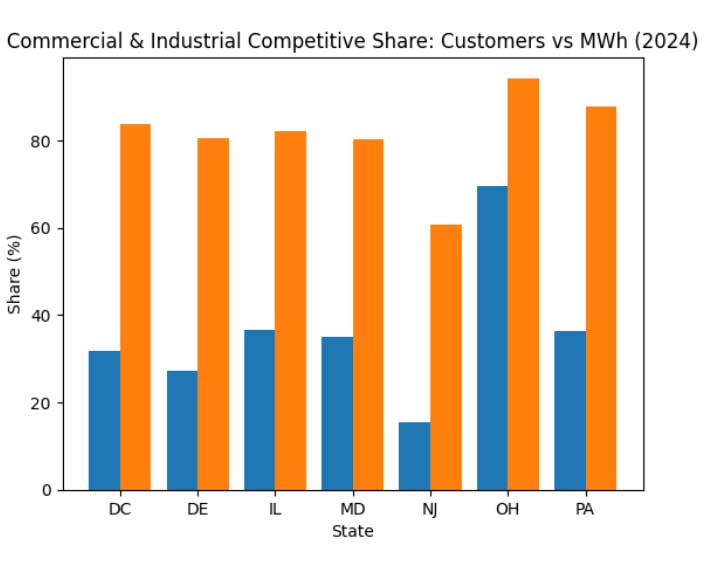

When measured this way, competitive suppliers now serve 80% to 90% of commercial and industrial electricity demand across many PJM states, including Pennsylvania, Ohio, Illinois, Maryland, New Jersey, Delaware, and the District of Columbia.

In other words, while residential participation has grown gradually, the vast majority of electricity used by businesses is already supplied competitively.

This striking difference reveals a transformation in electricity procurement that is largely absent from the public debate over competitive energy markets.

Two Markets, Not One

In reality, competitive electricity systems have always operated as two very different markets.

The first is the commercial and industrial market, where businesses actively manage energy procurement. These customers typically employ energy managers or rely on brokers and consultants to evaluate wholesale market conditions, hedge price risk, and negotiate supply contracts.

The second is the residential market, where most households lack both the time and the expertise to navigate complex electricity supply options.

The difference between these two markets is striking.

In many PJM states, less than one‑third of residential customers purchase electricity from competitive suppliers, while the overwhelming majority of commercial and industrial electricity demand is already served by competitive suppliers.

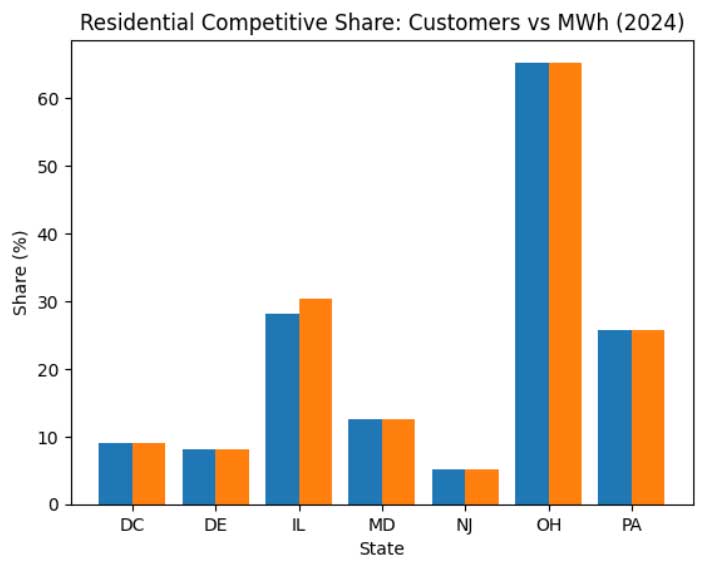

The following charts illustrate this contrast using 2024 market data. The first compares residential customer participation with residential electricity consumption served by competitive suppliers. The second compares the same metrics for commercial and industrial customers. Together, they highlight the fundamental structural differences between the residential and business electricity markets.

Figure 1. Residential Competitive Share — Customers vs MWh (2024)

Figure 2. Commercial & Industrial Competitive Share — Customers vs MWh (2024)

Footnote: Analysis based on U.S. Energy Information Administration EIA‑861 ‘Sales to Ultimate Customers’ data (2015–2024). Competitive share is calculated as electricity supplied by Retail Power Marketers divided by total electricity supplied by Retail Power Marketers and Investor-Owned Utilities providing bundled service.

Why Commercial Markets Flourished

Commercial electricity customers benefit from several advantages that residential customers historically lacked.

First, most businesses have access to detailed electricity usage data, often recorded in intervals of 15 minutes or one hour. This allows companies to understand when electricity is consumed and structure supply contracts accordingly.

Second, commercial customers frequently rely on professional energy managers, brokers, and consultants who specialize in electricity procurement. These experts monitor wholesale markets, analyze consumption patterns, and negotiate supply contracts on behalf of their clients.

Third, the scale of commercial electricity consumption makes procurement worth the effort. A large industrial facility may spend millions of dollars annually on electricity. Even small improvements in price can produce substantial savings.

These conditions created an environment where competition could function effectively.

Suppliers could design products tailored to specific load profiles, while buyers had the expertise to evaluate those offers. The result is the highly competitive commercial electricity markets that exist today.

Why Residential Markets Have Lagged

Residential electricity markets evolved under very different conditions.

Most households historically received only monthly electricity usage totals, providing little insight into when electricity was consumed. Without detailed usage information, it is difficult for customers to evaluate electricity supply offers or understand how different pricing structures might affect their bills.

At the same time, residential customers typically lack access to professional procurement expertise. While commercial buyers rely on energy managers, brokers, and consultants to guide purchasing decisions, households must evaluate electricity offers on their own.

But there is another powerful constraint that is often overlooked.

For more than a century, electricity service in the United States was provided by vertically integrated monopoly utilities. Customers had no choice of supplier, and the local utility became synonymous with reliability and safety. Generations of consumers grew accustomed to the idea that remaining with the local utility was the safest and most prudent choice.

Even after competitive energy markets were introduced, that perception remained deeply ingrained in consumer behavior. For many households, selecting a different electricity supplier still feels unfamiliar or risky. Many residential customers continue to view the utility’s default supply as the “safe choice,” even though default service prices are often established through procurement auctions that may produce higher costs than competitive alternatives.

An additional misconception surrounding residential electricity markets involves the role of utility default service. Many customers assume that the utility’s default supply represents the lowest‑cost option available. In reality, default service prices are typically established through periodic wholesale procurement auctions designed to ensure reliable supply rather than to deliver the lowest possible retail price at all times.

The Next Phase of Competitive Energy Markets

That situation is now changing rapidly.

Over the past decade, utilities across the United States have deployed AMI household meters that record electricity usage in detailed intervals. These meters generate the same type of granular consumption data that commercial energy managers have relied on for years.

At the same time, advances in data analytics, artificial intelligence, and automated procurement platforms are beginning to transform how residential electricity plans are shopped and bought.

These technologies are doing something that was not previously possible: bringing transparency to both sides of the residential retail electricity market.

For customers, detailed interval data allows households to understand how and when electricity is used in their homes. For suppliers, the same data allows electricity providers to develop pricing structures that reflect actual consumption patterns rather than relying on broad averages.

The result is the potential for customized electricity pricing at the household level.

Artificial intelligence systems can analyze interval usage data, monitor wholesale electricity markets, and automatically evaluate competitive supply options. In effect, these systems can function as automated energy managers for households, replicating the services that brokers and consultants currently provide to commercial customers.

The End of Traditional Retail Sales Channels

This technological transformation will also reshape how electricity suppliers reach customers.

Historically, residential retail electricity markets relied heavily on door‑to‑door sales, telemarketing, and call centers to acquire customers.

But as automated energy procurement platforms become more widespread, these traditional sales channels are likely to decline.

Door‑to‑door sales representatives and telemarketing campaigns are rapidly fading away in most markets. Over time, these methods will disappear entirely—much like the traveling Fuller Brush salesmen of earlier eras.

The future of residential electricity shopping will rely less on sales tactics and more on transparent pricing algorithms, automated platforms, and data‑driven energy services.

A More Accurate Perspective on Competitive Energy Markets

The history of competitive electricity markets is often framed as a failure because residential participation developed more slowly than expected.

But this interpretation overlooks the remarkable transformation that occurred in the commercial and industrial sector.

For large customers, competitive energy markets have delivered exactly what policymakers envisioned: a dynamic market where suppliers compete for customers, pricing reflects wholesale market conditions, and buyers have access to sophisticated procurement strategies.

The two charts presented earlier illustrate this clearly. Residential participation remains modest. In contrast, the commercial and industrial sector shows dramatically higher levels of competitive supply when measured by electricity demand.

As smart meter data, artificial intelligence, and automated procurement platforms continue to develop, households may finally gain access to the same analytical tools that commercial energy managers have used for years.

When that happens, residential electricity markets will finally begin to resemble the highly competitive commercial markets that already exist today.

=============================

About the Author

Dan Sullivan is a Marketing expert with more than three decades of experience across Competitive Retail Energy, Consumer Packaged Goods, and Technology. He spent over twenty years developing customer acquisition and market growth strategies in Competitive Energy Markets and later led Marketing and Brand initiatives in CPG and technology sectors. Dan is part of Heights Group Consulting.