Feature Articles

Have a topic request or want to submit an article? Contact the MAGNIFYI Editors

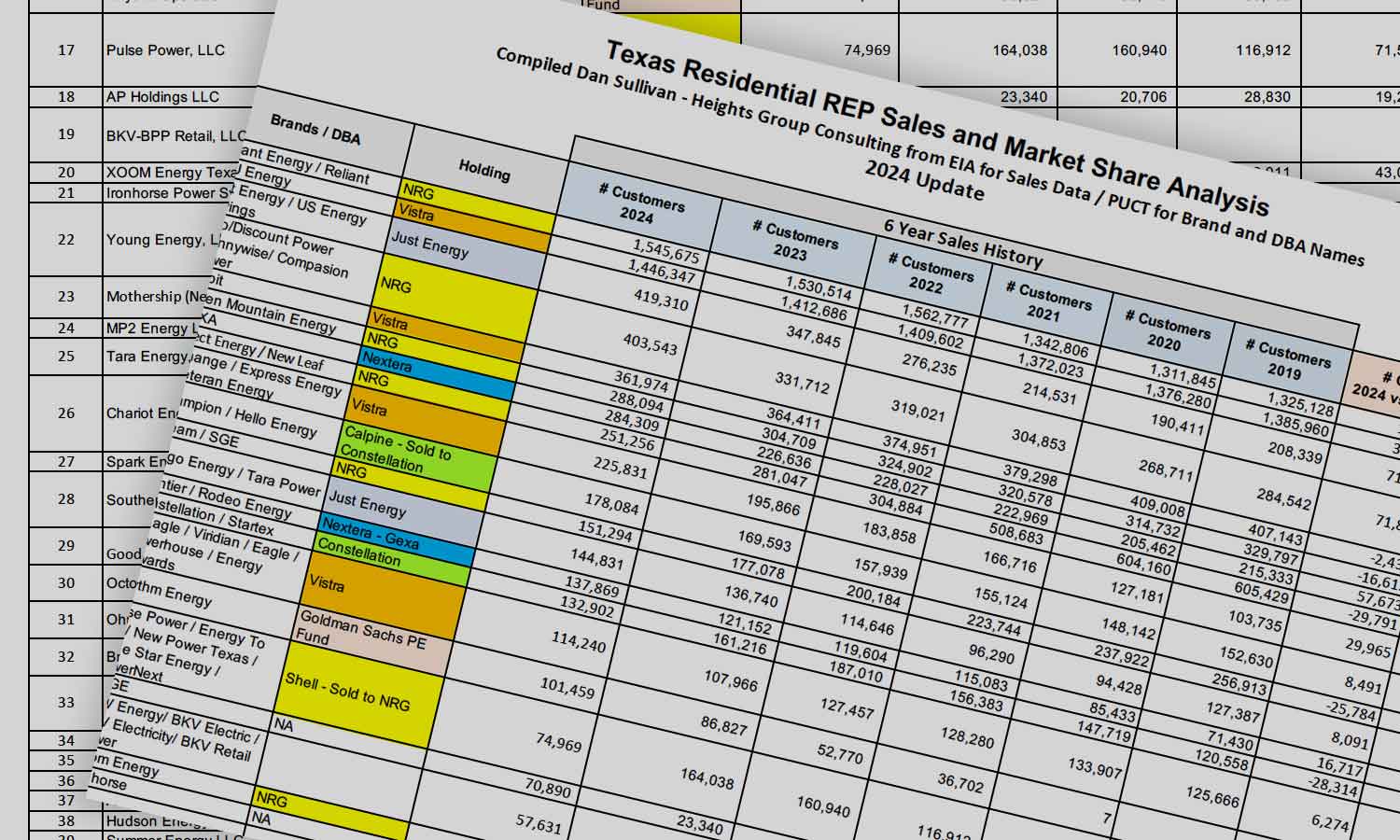

Battle of the Balance Sheets: The New Reality of Competition in Texas Retail Energy

What six years of market share data reveals about consolidation, competition, and the evolution of the Texas market.

Six years ago, I built a simple report.

The goal was straightforward: track annual residential sales of Retail Energy Providers in Texas and calculate market share to answer a basic question:

Who’s winning? And who’s losing?

Over time, as additional years of data were added, something more interesting began to emerge.

The spreadsheet stopped being a scoreboard.

It became a story.

Not just about individual companies—but about how the entire industry has evolved.

Today, I find myself looking at this data less through the lens of individual performance and more through what it reveals about the macro and micro forces shaping the market.

My hope is that you, as a reader, will find these insights useful in thinking about your own strategy, whether from a marketing, operational, or investment perspective.

Competition Evolved…It Didn’t Disappear

At first glance, a deeper look at ownership concentration in Texas appears to challenge a conclusion I shared in a previous MAGNIFYI article (Published 3/20/26) that market concentration has declined over time.

It doesn’t contradict that conclusion.

It refines it.

At the brand (Entity) level, the data clearly shows that concentration has declined over the past decade. Market share has spread across more brands, more offers, and more visible competitors. That’s the reality consumers experience and it’s real.

But when viewed at the ownership level, a very different picture emerges.

A growing share of those brands are owned by a smaller number of holding companies.

So, which is it?

The answer is both.

Competition in Texas has not decreased, it has changed form.

From Brand Competition to Portfolio Competition

In the early years of the market, competition was driven by:

- new entrants

- independent brands

- rapid expansion

Today, competition is increasingly driven by:

- scaled players

- multi-brand portfolios

- targeted segmentation strategies

Companies like NRG and Vistra are not competing with a single brand.

They are competing with:

- multiple brands

- multiple price points

- multiple customer segments

- multiple acquisition channels

What appears to be fragmentation at the surface is often intentional segmentation under a common owner.

What the Data Reveals About Market Evolution

Looking across the full dataset, several key takeaways emerge.

1. The market is consolidating despite visible brand proliferation

There are still dozens of brands in the market.

But at the ownership level, a small number of players control an increasing share of customers.

What looks like competition is often portfolio strategy.

2. The Top 2 players still anchor the market

Reliant (NRG) and TXU (Vistra):

- together control roughly 43% of the residential market

- a level that has remained remarkably stable over time

Despite all the change beneath them, the top of the market has shown durability, not disruption.

3. Growth at scale is driven by acquisition, not just competition

Much of the growth among leading players has come from:

- book-of-business acquisitions

- customer transfers from exiting suppliers

This is not purely organic competition.

It is consolidation-driven growth.

4. Mid-tier gains reflect redistribution, not expansion

Several mid-tier players have gained share.

But those gains are largely coming from:

- supplier exits

- customer reallocation

Not from a significant increase in overall switching behavior.

5. The long tail of competitors is shrinking

One of the most telling data points:

26 entities have ceased selling and report zero residential sales

These represent:

- exits

- inactive participants

- or failed scaling attempts

Entry is relatively easy. Building a sustainable business is not

6. Fewer players, stronger competition

The number of certified REPs suggests a broad field.

The reality is more concentrated.

A smaller group of scaled companies now competes more aggressively:

- with capital

- advanced marketing

- and sharper customer focus

As customers become more informed, the bar continues to rise.

Competition hasn’t weakened. It has intensified.

7. Brand choice remains high even as ownership concentrates

From a customer perspective:

- choice remains broad

- offers remain diverse

- pricing structures continue to evolve

Consumer choice has not declined even as ownership has consolidated

8. Entry is still possible—but sustained success is increasingly difficult

The data shows continued evidence of:

- new brands entering the market

- smaller players attempting to scale

But the growing number of exiting entities and the churn in the lower tiers suggest a clear pattern:

While the Texas market remains open to entry, it is increasingly unforgiving to those without scale, capital, and a clear strategy.

This is an important distinction.

The market is not closed.

Barriers to entry are still relatively low.

But:

- customer acquisition costs

- collateral requirements

- and competitive pricing pressure

Make long-term success far more challenging than in the early years of the market.

9. Beneath stability lies constant churn

The top of the market is stable.

Below that:

- suppliers exit

- books are sold

- new entrants attempt to scale

The market is dynamic underneath a stable structure.

10. Scale has become the defining advantage

The data points to a clear conclusion:

Success in Texas increasingly requires:

- capital

- operational efficiency

- customer acquisition scale

- risk management capability

This is no longer a market where small players can easily compete long-term.

A More Complete Definition of Competition

The deeper insight from this analysis is this:

Competition should not be measured solely by the number of suppliers—but by the range of meaningful choices available to customers.

Texas continues to deliver that.

What has changed is who is providing those choices—and how.

The Bottom Line

What initially appears to be a contradiction is actually a hallmark of a maturing market:

- Early phase: fragmentation and entry

- Growth phase: expansion and experimentation

- Mature phase: consolidation and scale

- Current phase: portfolio-driven competition

Texas has simply progressed further along this curve than most markets.

And that evolution should not be mistaken for a loss of competition.

It is a sign of a market that is working.